Getting to 100% Participation: Withholding Beats Payroll Deduction!

Jack Towarnicky, Of Counsel, Koehler Fitzgerald, LLC

Jack Towarnicky has spent nearly five decades helping to shape America's retirement landscape—from leading benefits strategy at Fortune 500 companies to serving as Executive Director of the Plan Sponsor Council of America—currently serving as Of Counsel at Koehler Fitzgerald, LLC. Jack recently completed his second three-year appointment with the Department of Labor, Employee Benefits Security Administration’s ERISA Advisory Council. His work includes converting thrift savings plans to include 401(k) deferrals and adopting bleeding-edge, pre-PPA’06 automatic features 20 years ago. When federal auto-IRAs were first proposed, he suggested a unique alternative, embracing 21st Century functionality. Towarnicky believes state auto-IRAs are suboptimal. Building on decades of plan sponsor experience, he advocates for a solution he calls "100% Participation." Jack would avoid individual and employment mandates, avoid adding payroll deduction, disclosure, and government reporting requirements, in favor of a withholding-based process that would reach every wage earner in America, not just those whose employers do not offer retirement plans, and only in states that do not have a mandated auto-IRA. In a season of retirement security focus, let’s learn more!

The State of Retirement in 2026

IRSM: Jack, thank you for joining us today. Let's start here: As we begin 2026, how would you summarize the effectiveness of our current retirement system?

Jack Towarnicky: Well, we've made real progress, ICI reports year-end 2024 retirement plan assets of $44+ Trillion. However, we still have significant gaps. On the plus side, automatic enrollment has been transformative. When I started, voluntary 401(k) participation rates were around 60% of eligibles. Now, with automatic enrollment, we're seeing participation rates above 90% in plans that use it. That's powerful evidence that practical applications of behavioral economics succeed.

We've also seen meaningful legislative progress to expand coverage to long-term part-time workers.

Jack notes that we're now seeing states step in with Auto IRA programs—Oregon, California, Illinois, and many others—ostensibly, their goal is to try to fill the coverage gap. On a pass-fail basis, Jack grades out the state auto IRA programs as a pass—based on increased IRA participation. But, in terms of retirement preparation effectiveness, he scores them as a D-.

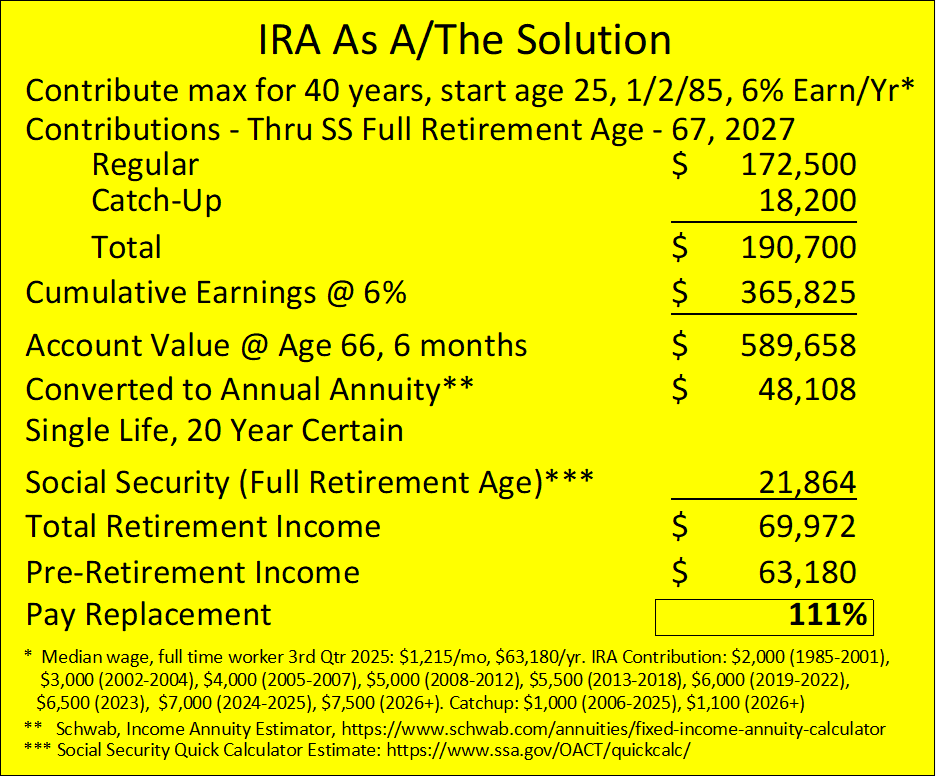

But here's the fundamental problem: According to the IRS, only about 12% of households contribute to IRAs today, even though IRAs have been universally available since 1982. We got off to a rousing start, but, while the Tax Reform Act of 1986 did not affect eligibility to contribute to an IRA, it adjusted the tax preferences. As a result, contributions declined by over 60% from 1986 to 1987. Think about that. We've had this vehicle for over 40 years, and participation has remained stubbornly low.

So, we have a universal option that is a more than adequate, tax preferred retirement savings program for all but the highest paid American workers.

Jack notes: “We don’t have a coverage or an access issue. We have an effective access challenge, perhaps a prioritization issue.”

The other major negative is leakage. Oregon was the first state-mandated IRA. If Oregon’s experience is typical, more than a third of all contributions to state-mandated Roth IRAs have already leaked out. As of December 2025, OregonSaves contributions totaled $561+MM, withdrawals totaled $219+MM, nearly 40%!

People cash out retirement savings when they need money—from IRAs, in-service or hardship withdrawals, and after separation when employment ends. Leakage continues to be a significant issue despite all our efforts to encourage preservation of retirement savings. Median tenure of American workers has been less than five years for the last seven decades. As a result, in the majority of employer-sponsored plans, and in all IRAs, once employment ends, the only liquidity option is a distribution. We haven't adapted our plans and retirement systems to match how people actually work.

The State Auto IRA Experiment: Promising But Limited

RSM: We've seen Auto IRAs begin to take hold and increase access through state mandates, but you think better ideas exist. What are your thoughts on a 100% participation solution?

JT: I think the state Auto IRA programs have been well-intentioned, but when you look at the actual results, they're disappointing. Let me give you some specific numbers. In OregonSaves, which is often held up as the model, as of December 2025, over 26% of auto enrolled workers have opted out. Those who contribute save a median monthly amount of $153, roughly $1,836 a year. If you project that out over a 35-year career—say, age 32 to Social Security retirement age of 67—you're talking about total contributions of about $64,260.

Now, with a 2% real rate of return after inflation, after fees, you end up with about $83,250 in purchasing power. That's a very modest outcome. And that's assuming everything goes perfectly—no job changes, no relocation across state lines, no opt-outs, no withdrawals for emergencies. And, that’s the median, more than half will have less, many will have much less.

Compare that to what's available in the private IRA market. Fidelity, for example, offers IRAs with zero administrative fees. You can invest in index funds with next to zero asset management fees. The cost difference is enormous, and it compounds over time.

But the bigger structural problems with state Auto IRAs are even more significant. First, they only reach workers whose employers don't offer plans. So, if you work for an employer that has a 401(k), but you're not eligible because you're part-time, or you haven't met the service requirement, or you're in an excluded class of employees, the state IRA programs don't help you. You're still left out.

Same for those whose employer offers a defined benefit pension plan, where vesting typically occurs after 5 years (3 years for plans with cash balance formulas). Given that the median tenure of American workers has consistently been less than 5 years, even those who are eligible and participate may not vest.

Second, the Roth IRA mandates are state-specific. If you live in Oregon and get automatically enrolled in OregonSaves, then move across the river to Washington for a new job, you're not automatically re-enrolled. The system doesn't follow you. Your ability to save becomes dependent on which state you happen to work in.

Third, most state Auto-IRAs are "one and done." If you opt out at enrollment or later reduce your contributions to zero, many states don't prompt re-enrollment until you change employers. There's no perennial nudge, no annual reminder that saving matters.

Fourth, under current rules, Roth IRA assets from state programs can't be rolled into employer 401(k) plans. So, if you build up $15,000 in a state Roth IRA, then get hired by an employer with a great 401(k) plan, you can't consolidate those assets. They stay fragmented. Separate programs, separate fees, separate administration.

Fifth, most state programs use the Roth IRA vehicle. That vehicle allows withdrawal of Roth IRA contributions first, withdrawal at any time, withdrawal with no associated income taxes. So, in California for example, CalSavers highlights the following:

“… We keep it simple: you can take out your money when you need it. … While the program is meant to help you save for retirement, we understand that life has its ups and downs. What you do with your savings is entirely up to you, and the money you save is available to you if you need it in an emergency. If you only take your contributions out there are no taxes or penalties. …”

A Different Approach: 100% Participation Through Federal Withholding

JT (continued): What I've been advocating instead—and I first proposed this back in November 2007—is a system I call "100% Participation." The core idea is to leverage existing federal income tax withholding requirements instead of payroll deduction.

Think about it: Every employer in America already complies with federal income tax withholding. Every payroll system already remits money to Treasury electronically. The infrastructure exists, the civil and criminal penalties for non-compliance exist, the annual update process exists. We don't need to build something new or impose new mandates on employers.

But most important: The vast majority of American households are already exhibiting “savings” behavior through the income tax withholding process. Would you be surprised to hear that as of December 25, 2025:

There were 154,911,000 tax returns filed electronically,

Of that number, 103,846,000 households received a refund,

94,335,000 of those refunds were processed electronically/direct deposited into a bank account, and

The average direct deposit refund was $3,230!

In fact, in every one of the last 12 years, that same pattern applied—100+MM returns, 100+MM returns with refunds, which averaged $2,800+ in each and every year!

Here's how it would work: For workers who aren't currently contributing to an employer-sponsored plan (per box 12, form W-2) as of November each year, supplemental federal withholding would apply—to increasing the amount withheld each payday. Workers would receive a notice in November of any change in withholding that would be effective in January of the following year. But this isn't a forced contribution. Workers can prospectively change their -4 at any time.

Then, every year when filing the tax return, every taxpayer using e-file software would be prompted to contribute to an IRA. The software would show them the options—traditional deductible IRA or Roth IRA. It would calculate and display the Saver's Match if they qualify. And they'd have a "last clear chance" to make the final decision: contribute some or all of the refund to an IRA, contribute more than the available refund, or take the full refund.

This creates what I call "perennial nudges." You're being prompted to save at least twice a year, every year, regardless of whether you maintain your current employment. You get a notice in November about your withholding, then you get prompted again when you file your taxes. That's twice a year, every year, for your entire working life.

“Only about 10% of workers contribute to IRAs today, even though IRAs have been universally available since 1982. The system works for those who join an employer with a plan, who save and remain with that one employer, but that’s only a very small minority of American workers.”

The Mechanics: How It Works

RSM: Walk us through the mechanics. How would this work in practice?

JT: Let's start at the beginning—when someone is hired. The employer would provide a notice explaining the default withholding rules and give the employee an opportunity to complete a W-4 form. For workers who will be eligible to participate in an employer-sponsored plan within three months of hire (or by the following April 1st if hired late in the year), the withholding default would be the standard: single, zero allowances. For workers who won't be eligible for an employer plan, the default would be the same plus supplemental withholding.

The supplemental withholding amount would be set by Treasury, and I've proposed starting at 5% of the median full-time wage—which today would be about $2,500/year — and increasing it $25, $50, or $100 a year until it reaches the maximum. That creates a gradual ramp that encourages higher savings over time.

Now, every November, workers who are not contributing to an employer-sponsored plan would be subject to supplemental withholding, and would receive a notice from Treasury confirming the withholding amount for the coming year and reminding them of their right to adjust it. They can submit a new W-4 at any time if they need to change their withholding.

Then comes the key part: tax filing. When you prepare your return using e-file software—and remember, over 90% of refunds are now filed electronically using electronic banking, the software would present the IRA contribution option prominently.

It would show your calculated refund and suggest an IRA contribution amount—typically the lesser of your refund or the maximum IRA contribution for that year. It would show you side-by-side comparisons: "Here's your refund with no IRA contribution. Here's your refund if you contribute $X to a traditional deductible IRA. Here's your refund if you contribute $X to a Roth IRA." It would calculate the Saver's Match automatically and show you the impact.

You'd then have three choices: accept the default contribution, adjust the amount up or down, or decline the IRA contribution and take your full refund. You'd also choose whether you want a traditional or Roth IRA, and you'd select from a list of pre-qualified IRA vendors—what I call the "connector" system—or let Treasury assign you to a default vendor.

The beauty of this is that it works with the grain of existing taxpayer behavior—regardless of whether the individual is eligible for and/or contributing to an employer-sponsored plan. We already have more than 100 million Americans receiving refunds every year, averaging over $3,000. These are people who have demonstrated they can live on less than their full paycheck—they've been over-withholding all year. We're just giving them an easy, visible option to redirect some of that over-withholding into retirement savings.

“When you file your tax return, the default would be to direct a portion of your refund to an IRA. The software would show you the tax impact, explain the Saver’s Match if you qualify, and give you the choice. You’re being prompted twice a year, every year.”

Addressing the Coverage Gap, Leakage, and Complexity

RSM: How would this address the current challenges in the system—things like coverage gaps, leakage, and the complexity you mentioned?

JT: Let me tackle each of those.

On coverage, this process reaches literally every wage earner—whether or not eligible for an employer plan. That includes people working for small businesses that don't offer plans, yes, but also people who are excluded from their employer's plan because they're part-time, because they're hourly workers in a class that's excluded, because they haven't met the age or service requirements yet, or because they're seasonal workers. It also reaches gig workers, self-employed people, and workers whose employers have non-contributory plans where employees aren't allowed to contribute. Finally, workers who are eligible for and contribute to an employer-sponsored plan can also leverage this IRA process.

State Auto IRAs miss all of these people. A state program typically says, "If your employer doesn't offer a plan, you're covered." But that leaves out tens of millions of workers whose employers do offer plans, but who aren't personally eligible as well as those who are eligible but who do not contribute. My proposal covers everyone not currently eligible to participate and those eligible but not contributing to an employer plan.

On leakage, the key is that this system creates accounts that follow workers across jobs and across state lines. When you change employers, your IRA stays with you. Whether or not your next employer offers a plan, whether or not you are eligible, you can continue contributing to the same IRA. If your new employer does offer a plan and you become eligible, you could potentially roll your IRA assets into that plan—especially if the plan includes what are called "deemed Roth IRA" provisions under Section 408(q) of the tax code.

Deemed IRAs, by the way, are an underutilized feature that allows 401(k) plans to accept IRA contributions and IRA rollovers within the plan structure. This creates a vehicle for true asset aggregation. Imagine you've built up $15,000 in a Roth IRA through the withholding system, then you get hired by an employer with a good 401(k). Instead of having your money scattered across multiple accounts, you could consolidate everything into your employer's plan, benefit from institutional pricing and loan provisions, and build a more substantial retirement account.

The withholding system also addresses leakage in another way: It creates perennial prompts to save. Even if someone opts out of contributing one year, they'll be prompted again the next year. We know from research on automatic enrollment that people often make different decisions when re-prompted. Someone who opts out at age 25 might opt in at age 30 when their circumstances have changed.

And because the prompts happen at tax time, when people are already thinking about their finances and seeing their full financial picture for the year, the timing is psychologically optimal. You're not asking someone to make a savings decision in isolation. You're asking them to make it at a moment when they're reconciling their annual income, deductions, credits, and refund. That context matters.

On complexity, we're actually simplifying things, not adding complexity. Think about what we have now: 50 states potentially creating 50+ different state and local Auto IRA systems, each with different rules, different vendors, different fee structures, different eligibility criteria. That's incredibly complex, especially for workers who move across state lines or for employers who operate in multiple states.

What I'm proposing uses systems that already exist and that every American already interacts with: income tax withholding, the W-4 and W-2 forms, the 1040 tax return, electronic fund transfers. The IRS already processes over 150 million individual tax returns every year. Treasury already handles billions of dollars in electronic fund transfers. We're not building new infrastructure—we're using what we have more intelligently.

And for IRA vendors, this is far simpler than the state-by-state approach. Instead of having to comply with Oregon's rules and California's rules and Illinois' rules, each slightly different, they'd comply with one federal standard. Instead of receiving contributions weekly or bi-weekly from thousands of small employers, they'd receive one annual contribution directly from Treasury with complete taxpayer information. The economies of scale are enormous, which is why I'm confident this would result in very competitive, low-cost IRA products.

Fitting Into (and Improving) the Existing System

RSM: How would this fit into the existing system? Would it replace Auto IRAs? What happens to 401(k) plans?

JT: This would complement the existing system, not replace it. The 401(k) system, for those it covers, is actually quite good. The problem is who it doesn't cover and how it handles job changes. This proposal fills those gaps.

For 401(k) plans, nothing would change directly. Employers would still design their plans as they see fit. Employees who are eligible would still participate. The automatic enrollment provisions we've spent years implementing would still work.

But here's what might change, and I think it would be a positive change: If high-quality, low-cost IRAs become readily available to every worker through this federal system, it creates competitive pressure. Workers might start asking their employers, "Why do I have to pay 1% in fees when I can get a Fidelity IRA for free? Why do I have to wait a year before I'm eligible when I could be saving in an IRA right now? Why does my 401(k) limit me to these 20 investment options when I could have self-directed investing in an IRA?"

That competitive pressure could drive improvements in employer plans. Lower fees, earlier eligibility, faster vesting, better loan provisions, more investment options. That's healthy competition that benefits workers.

I've been advocating for years that 401(k) plans should position themselves as what I call "asset magnets." Instead of being solely focused on retirement and then pushing people out when they separate from employment, plans should make themselves attractive places to consolidate assets from IRAs and prior employer plans and subsequent employer-sponsored plans, too! That means competitive fees, good investment options, facilitating “rollovers” of outstanding, defaulted loans, 21st Century loan functionality for liquidity, and clear communications that you can stay in the plan indefinitely after separation.

Think about the value proposition of a good 401(k). If you save on a pre-tax basis, if your employer matches 50% of your contributions, and if you are in a 20% federal and state marginal income tax bracket, for every $.56 reduction in your take home pay, you defer $.14 in federal and state income taxes, and receive a company match of $.30, resulting in a $1.00 addition to your account. That's incredible. When I presented my 401(k) plan to workers, on their first day on the job, I presented this as part of a “magic show.” The goal was to confirm to workers that they worked here, and that they could perform this same trick every payday.

Workers could continue their state Auto IRAs. However, the federal rules would also apply. Right now, we're seeing states spend considerable resources building parallel systems that duplicate existing IRA infrastructure. OregonSaves, CalSavers, Illinois Secure Choice—they're all trying to solve the same problem with slightly different approaches, and none of them reach everyone who needs to save.

A federal solution would be more efficient, more comprehensive, and would avoid portability issues. It would provide uniform coverage regardless of which state you work in. And it would leverage the existing IRA infrastructure that Fidelity, Vanguard, Schwab, and hundreds of other firms have already built, rather than requiring states to build new systems from scratch.

The federal government has a role here, just as it did with Social Security and Medicare. Retirement security is a national issue. The patchwork of state programs creates inefficiency and leaves gaps. We need a national solution.

Beyond Access: Liquidity Without Leakage

RSM: You've mentioned several times that this would work better with some enhancements to IRAs. Can you elaborate on those?

JT: Absolutely. This isn't just about creating a better on-ramp to retirement savings. We also need to make the vehicles themselves work better, particularly around liquidity and leakage.

Let me start with a fundamental concept: liquidity without leakage. The single biggest barrier to retirement saving is that people don't think they can afford to lock money away until age 59½. They have immediate needs—car repairs, medical bills, helping family members, dealing with income disruptions. If retirement savings are completely illiquid, many people simply won't participate, or they'll contribute less than they should.

The solution is to provide the “right” kind of liquidity and discourage the “wrong” kinds of liquidity. The “right” kind of liquidity is a loan—most loans from employer-sponsored plans are repaid. The “wrong” kind of liquidity is a withdrawal—most withdrawals from employer-sponsored plans are never repaid.

Right now, 401(k) plans can offer loans, but IRAs cannot. That's a huge disadvantage for IRAs. I've been advocating for years that Congress should extend loan provisions to IRAs on the same terms as 401(k) plans.

Now, Congress has been going in the wrong direction. SECURE 2.0 added all kinds of new penalty-free withdrawal provisions—emergency expenses up to $1,000 annually, domestic abuse situations, terminal illness, disaster relief. These are well-intentioned, but they increase leakage.

What we should be doing instead is making loans more accessible and easier to use? Here are the changes I'd propose:

First, electronic banking. Most Americans pay at least one bill electronically each month. Why not 401(k) loans? Obviously, loan repayment can continue after separation, reducing leakage. Further, loans could be initiated after separation. Think of the value to term vested participants—remember, more than one in five 401(k) accounts belong to someone who is term vested or retired!

Second, line-of-credit structure. Let people borrow only what they need, when they need it, rather than taking more than needed because the plan only permits one loan at a time.

Third, portability of loans between plans. If you change employers and your new employer's 401(k) offers loans, you should be able to rollover the residual balance, then take loans from the receiving employer-sponsored plan to complete the rollover of your entire account balance. The Tax Cuts and Jobs Act of 2017 extended the period to roll over loan offsets from 60 days to the tax filing deadline, which helps with the timeline for processing.

Two other changes, allocating the interest the government saved because of supplemental withholding:

First, for those who had supplemental withholding, and contributed those monies to an IRA, a credit of interest equal to the interest the federal government saved due to supplemental withholding, and

Second, creating a prize-linked IRA contribution by taking the interest saved on federal debt from supplemental withholding for those who did not contribute to an IRA—an annual drawing with an award of a full year’s contribution.

These changes would transform 401(k) plans and IRAs from being solely retirement vehicles into being financial wellness tools. You could accumulate assets for retirement, but you could also access them for genuine needs along the way, with a structure that encourages repayment and minimizes leakage.

The evidence shows this approach works. Most plan loans are repaid successfully. Default rates are relatively low, especially for smaller loans and when repayment can continue after job separation. And when you look at the alternatives people use—credit card debt at 20% interest, payday loans at 400% APR, or just going without needed medical care or car repairs—plan loans are far superior.

Jack notes: I’ve written a number of articles on why plan sponsors (and IRAs) should favor loans over withdrawals. Feel free to connect with me on Linked in and ask for electronic copies.

The IRA Connector: A Marketplace Model

RSM: You mentioned a "connector" system for IRA vendors. How would that work, and what would the standards be?

JT: The connector would function like a marketplace of pre-qualified IRA vendors—think of it as similar to the Medicare Part D model or the old healthcare exchange concept, but simpler.

Here's how it would work: Treasury would issue a request for proposals annually, setting minimum standards that vendors must meet to participate. These standards would include things like:

First, fees. The goal should be zero or very low administrative fees. No setup fees, no annual maintenance fees, or fees so low they're clearly competitive. We want to maximize what participants keep.

Second, investment options. Vendors would need to offer simple, low-cost default options like target-date funds or balanced funds but also provide self-directed brokerage for those who want it. Ideally, some options would have zero asset management fees—index funds that are essentially free with no tracking error.

Third, electronic integration. Vendors would need to be able to receive contributions directly from Treasury via electronic transfer and provide participant access via web and mobile platforms. They'd also need to support ACH transactions for loan repayments if the person separates from an employer.

Fourth, participant education and support. When someone makes their first contribution, the vendor should reach out within days—not weeks or months—to help them choose investments if they haven't already, and understand their options. First-time savers especially need support.

Fifth, portability. Assets must be easily transferable to other qualified IRA vendors without fees, and Traditional IRAs would be capable of rollover into employer 401(k) plans where allowed. We don't want to create sticky accounts that trap people in suboptimal arrangements.

Treasury would evaluate the proposals and select maybe a dozen qualified vendors—enough for meaningful choice and competition, but not so many that it's overwhelming. The selection would be refreshed periodically to ensure ongoing quality.

If you contribute to an IRA through the tax filing system but don't select a vendor, you'd be assigned to a default vendor from the pre-qualified list, probably on a rotating basis to spread the volume. But you'd have 60 days to transfer your assets to a different qualified vendor at no cost if you wanted to change.

This is important: We're not creating a government-run IRA program. We're leveraging private sector competition and existing IRA infrastructure, but with Treasury acting as a gatekeeper to ensure quality, low cost, and consumer protection.

Addressing the Paternalism Critique

RSM: What about the critique that this is too paternalistic—that it's forcing people to save?

JT: I hear that concern, but I think it misunderstands what this proposal actually does. Nobody is forced to contribute to an IRA. Let me be very clear about that.

First, the supplemental withholding can be adjusted at any time by submitting a new W-4. If someone doesn't want the extra withholding, they can stop it immediately. Second, at tax time, when you file your return, you make the final decision about whether to contribute to an IRA. You can decline and take your full refund. You're always in control.

Now, is there a default? Yes. Does the default encourage saving? Yes. But defaults aren't the same as mandates. We use defaults all the time in retirement plans—automatic enrollment in 401(k)s is a default. Nobody calls that forcing people to save because people can opt out.

What we're really talking about is choice architecture. The question isn't whether we should have defaults—we always have defaults, even if the default is "do nothing." The question is what the default should be. Should the default be that you take your full refund and spend it? Or should the default be that you save some of it for retirement, with an easy option to override that default if you want?

I would argue that nudging people toward saving is appropriate public policy. Most people, when surveyed, say they wish they saved more. They have good intentions but struggle with follow-through because of present bias—immediate needs feel more urgent than distant retirement. By making the default to save, but keeping it fully reversible, we're helping people act on their own stated intentions.

This isn't paternalism in the sense of overriding people's choices. It's paternalism in the sense of designing systems that help people achieve their own goals, as they define them. There's a big difference.

And consider the alternative. We already have paternalistic elements throughout our system. Social Security is mandatory—you can't opt out of FICA taxes. Many states now mandate Auto IRA enrollment through employers. Employers can automatically enroll workers in 401(k) plans. So, the question isn't whether we use automatic features—we already do. The question is whether we use them effectively.

What makes this different from state mandates is the transparency and control. With this system, you're being told upfront, "Supplemental withholding will apply unless you submit a W-4 to change it." You can change it immediately. Then at tax time, you get a clear choice with full information about the tax implications. Compare that to automatic payroll deduction, where money comes out of your check and you might not fully understand the tax treatment until much later. This is actually more transparent and puts more control in the hands of the worker.

I'd also point out that this addresses what economists call "present bias" without removing freedom of choice. Most people intend to save for retirement. When surveyed, they say they should save more. But they struggle to act on those intentions because immediate needs feel more pressing. Automatic features help bridge that gap between intention and action. That's not overriding people's preferences—that's helping them achieve their goals.

The Path to Enactment: Politics and Practicality

RSM: Let's talk about the politics and practicality of this. You first proposed this concept in 2007. Why hasn't it happened, and what would it take to get it enacted now?

JT: The 2007 proposal was an alternative to what became the Automatic IRA Act proposals that were circulating in Congress at that time. Those proposals would have mandated that certain employers set up payroll deduction IRAs. I was a plan sponsor then, heading benefits at a Fortune 100 company, and I could see the problems with that approach. New costs for payroll systems, new administrative and compliance burdens, potential fiduciary exposure, and it still wouldn't reach everyone.

The withholding alternative I proposed would have avoided all of that by using existing tax infrastructure. I discussed it with policy wonks at Brookings and Heritage, and folks at AARP. Everyone seemed to prefer their solution.

No surprise there. But here we are, 20 years later.

Instead, we got the state Auto IRA movement, which addressed the effective access issue (with the default, not the Roth IRA which was already in place)—creating the patchwork complexity I've described. And we got SECURE Act and SECURE 2.0, which made incremental improvements but didn't fundamentally solve the coverage gap, and incorporated provisions which, if widely adopted, will significantly increase leakage.

Why didn't the withholding approach happen? Several reasons. First, there's always resistance to changing tax withholding processes, even though we adjust withholding all the time for policy reasons. Second, the IRA industry wasn't focused on this opportunity. They've been much more focused on capturing rollover assets from 401(k) plans, which represent trillions of dollars. Third, there was political momentum behind employer mandates and then state solutions, so that's where the energy went.

However, as noted earlier, payroll deduction is sooooo 20th Century.

I think the conditions are actually much better now than they were in 2007. We now have nearly two decades of data on automatic enrollment showing it works. We have several years of data on state Auto IRAs showing their limitations—modest savings amounts, high fees relative to alternatives, narrow coverage, complications from state-by-state variation.

We have the SECURE Acts showing bipartisan appetite for retirement legislation. We have much better electronic systems for tax filing and fund transfers than we had 17 years ago. Over 90% of refunds are now direct deposited. Nearly all workers are paid electronically. The infrastructure is in place.

What we need now is a champion in Congress willing to introduce this as an alternative to expanding state mandates. The pitch would be: federal solution, universal coverage, no new employer mandates, uses existing infrastructure, lower costs, better outcomes. It should appeal to both parties.

Democrats would like the universal coverage aspect and the progressive elements like the Saver's Match being made more visible and effective. Republicans would like the lack of employer mandates, the private sector competition among IRA providers, and the individual control—workers can opt out, adjust their withholding, and make their own decisions.

The biggest obstacle would probably be opposition from states that have invested in their own Auto IRA programs. They'd see this as federal preemption of their efforts. But I'd argue that federal preemption is appropriate here, just as ERISA preempted state regulation of pensions. Retirement security is a national issue. We need a national solution that works regardless of which state you live in or work in.

I'd also note that the voluntary nature of this proposal should make it less politically contentious than a mandate. Workers retain full control through their W-4 elections and their tax filing choices. Employers have no new responsibilities beyond what they already do for tax withholding. It's a nudge, not a shove.

The Road Ahead: 2026 Priorities

RSM: Let's turn to your focus in 2026. What are you hoping to accomplish, and what would you like to see the industry and policymakers do?

JT: My primary focus is getting this 100% Participation concept in front of policymakers with the urgency it deserves. We've spent 20 years trying to increase participation, and while we've made some progress, we're still leaving too many people behind. We need a comprehensive federal solution.

Specifically, I'd like to see several things happen:

First, introduction of legislation that implements supplemental withholding for workers not eligible for employer plans and creates the IRA connector system. This could be positioned as building on what states have done—"Auto IRA Plus" or something that signals we're taking it to the next level.

Second, Treasury regulatory guidance that clarifies and encourages deemed IRA adoption by 401(k) plans. This provision has been in the law since the Economic Growth and Tax Relief Reconciliation Act of 2001, but hardly any plans use it. Why? Partly because there's been very little regulatory guidance on how to administer it. Plan sponsors are naturally cautious about adding features without clear rules. Labor and IRS should issue regulations and model plan language to make this easy in ways that would not increase the chances for plan disqualification or fiduciary violation.

Third, Congressional action to extend loan provisions to IRAs on the same terms as 401(k) plans. This is logical and would make IRAs far more attractive and useful. The arguments against it have always been about preventing retirement leakage, but as I've explained, properly structured loans will reduce leakage by providing access in a way that requires repayment.

Fourth, I'd like to see the industry adopt the "asset magnet" concept more broadly. Plan sponsors should stop pushing people out at job separation with involuntary distributions and automatic paperwork. Instead, make plans attractive places to keep assets and consolidate assets from IRAs and other plans. That means competitive fees, good investment options, strong loan features, and clear messaging that you can stay in the plan indefinitely. For example, Towarnickys will remain participants in the plan I designed in my last plan sponsor role, for 10 years after the second of us dies. I have been a participant in that plan for 37 years. Assuming typical life expectancy, I, my wife or my children will have been participants in that plan for 65 years!

Fifth, I think we need to reform some of the emergency withdrawal provisions in SECURE 2.0. I appreciate the intent—helping people deal with financial shocks—but the execution increases leakage. We should be steering people toward emergency loans from their retirement accounts, not emergency withdrawals.

Sixth, I'd like to see a broader conversation about financial wellness and retirement readiness that acknowledges that people have needs along the way to retirement, not just at retirement. The retirement industry has sometimes taken an absolutist position that any access to retirement savings before age 59½ is bad. That's wrong. The right position is that unplanned, unstructured access is bad, but planned, structured access through loans or other repayment mechanisms can actually improve retirement outcomes by reducing barriers to participation.

Reasons for Hope

RSM: This is ambitious. What gives you hope that we can actually accomplish this?

JT: Several things give me hope.

First, the demographic imperative. We have about 67 million Baby Boomers, most will have retired by 2035. Behind them are Gen X, Millennials, and Gen Z who have had even less access to traditional pensions. Second, incremental approaches aren't enough. We've tried employer mandates in some forms, we've tried state Auto IRAs, we've tried expanding 401(k) eligibility, we've tried the Saver's Match. All of it helps at the margins, but none of it solves the fundamental problem: Most Americans don't save enough for retirement, and when they do save, they often cash out.

Third, the infrastructure is in place.

Fourth, we've learned from the state experiments. OregonSaves, CalSavers, and the others have shown that automatic enrollment works—people will save if it's easy. But they've also revealed the limitations of state-by-state, employer-based approaches. We can do better.

Fifth, I'm hopeful because I've seen the retirement system evolve dramatically over my career. When I started in benefits in the late 1970’s, defined benefit pensions were more common. 401(k)s didn’t appear until 1982. IRAs had just become universal. I've watched automatic enrollment go from a radical idea to standard practice. I've seen contribution limits increase, fees come down dramatically, investment options expand. The system can change when there's will and evidence.

What we need now is leadership—someone in Congress, or at Treasury, or in the retirement industry to champion this and push it through. I'm not a legislator. I'm a practitioner and advisor. What I can do is suggest policy and plan design, share the evidence, and keep making the case.

I'm convinced this approach—using tax withholding to create perennial nudges to save, leveraging existing infrastructure, providing universal coverage without employer mandates, creating portability across jobs and state lines—is the best solution.

We have the tools, the technology, and the knowledge. What we need is the will to implement comprehensive solutions that work for every American, not just those lucky enough to have good employer plans.

RSM: Jack, thank you for sharing your insights and vision. This has been a great conversation today.

JT: Thank you, Lisa. I appreciate the opportunity to lay out these ideas in detail. Retirement security matters. It matters for individuals, for families, for communities, for our economy. We can do better, and I'm confident we'll get there.

Connect with me on Linkedin if you would like a copy of anything mentioned here.