The System America Deserves: A Conversation with Karen Andres and KC Boas of the Aspen Institute Financial Security Program

Karen and KC, you’re both deep in the work of making financial security real for people. What are your current priorities—let’s start with you, KC, on inclusive savings.

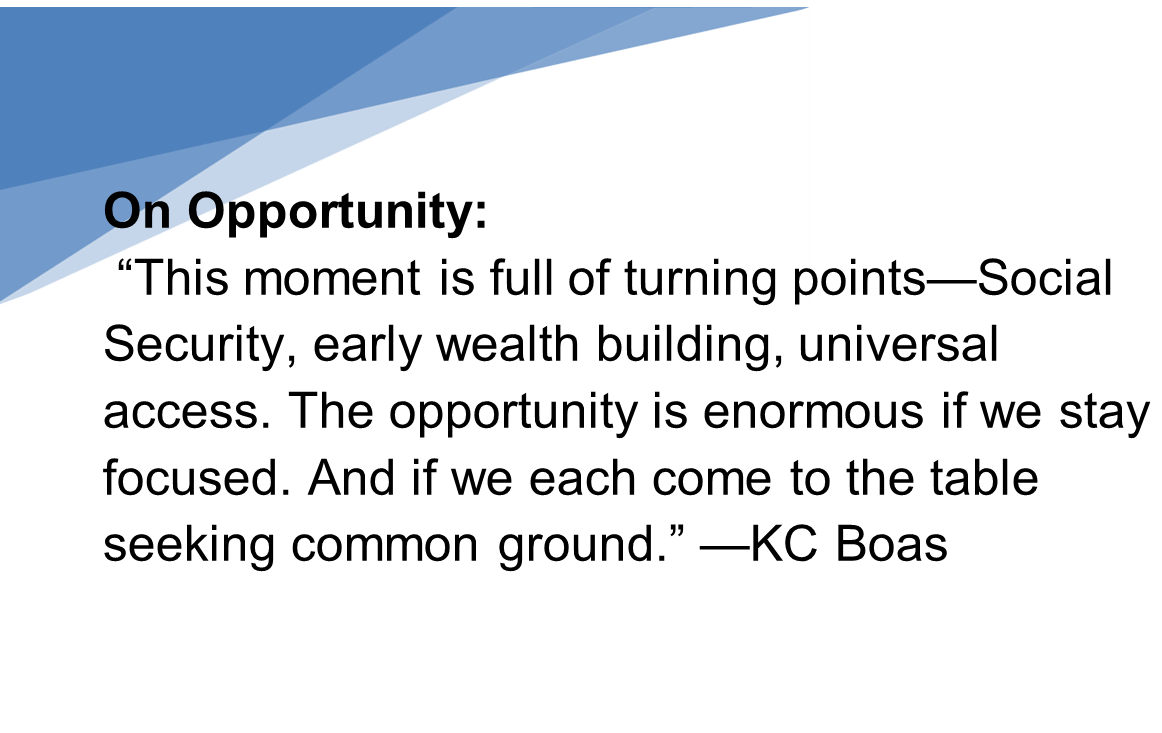

KC Boas: Yes—I’ll frame it this way. There’s a tension at the heart of this work: America’s retirement system is working for millions. And it’s failing millions. Both are true. But failure isn’t inevitable. The system isn’t working for many yet. And the “yet” is where we see opportunity.

Over the past few months, we’ve been scheming… Dreaming up what the next five years of our work needs to be. Our guiding principle was to start with the experience of the household. When you boil it down, the lifecycle of a retirement saver has three parts: access, saving & investing, and retirement.

So, we’re organizing our work around that journey. The Workers’ Wealth Lab, launched in 2024 with our partners at DCIIA and Morningstar, will continue to focus on how we can make the save-and-invest cycle work for everyone, regardless of income, profession, race, gender, generation, and more. Our work has always had access expansion as a core goal—and now we’re launching a new program: the Retirement Income and Affordability Lab—designed to tackle systemic failures for financially insecure households in this phase of the lifecycle.

You’re also planning a financial diaries project for older Americans. We learned so much from the first work. Tell us more.

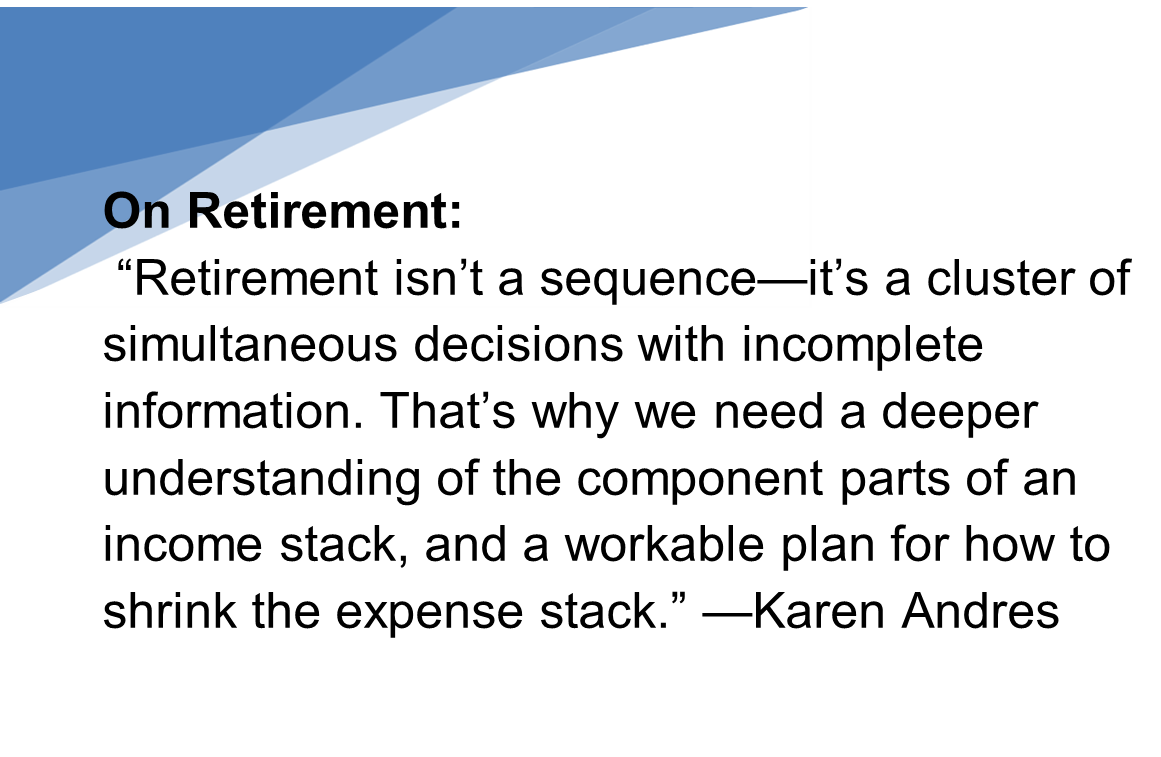

Karen: Yes. It’s a time-tested methodology that’s never been applied to older adults, so we’re breaking new ground. The appeal of this approach is that it marries real lived experience—I’m talking, sitting across from a retiree at their kitchen table and digging into the details of what’s happened in their financial life and why—with transactional data.

That’s what we plan to do with a sample of 100 low-wealth households, ages 55–75. What decisions and trade-offs are they making? How do they react to financial shocks? Where are the gaps? Uncovering the answers to these types of questions can drive better design of both policy and product. And this really matters given how close we are to a benefits cut for Social Security if policymakers don’t take action.

We’re in project funding, and looking for partners who want to help us press play.

Karen: They’re now the law of the land! There’s a lot to unpack there—and even more to figure out. As passed into law, these accounts are a traditional IRA—so, not a Roth—for all kids under 18, starting as early as birth, and who have a Social Security number.

But there are several unique features—like a $1,000 seed investment pilot program—some of which need to be clarified with the Treasury Department.

Over the past several months, we’ve held dozens of roundtables with 50+ stakeholders across sectors—and we’ve written extensively about those findings. But the bottom line is: we see Trump Accounts as a downpayment on a groundbreaking idea—that every kid should be endowed from birth with a lifelong investment account and a stake in the economy. A downpayment we’re eager to improve over time, just as we have with other bold policies in this country.

Is the link between these accounts and retirement important?

KC: Massively. And it’s important that we—as an industry—quickly embrace these accounts as retirement funds…because they are.

Think about the precedent that’s being set: a universal, portable approach to long-term savings.

The traditional IRA structure means these accounts can reach the 56 million private-sector workers who lack access to a workplace retirement plan, as well as the 16.5 million Americans who rely on independent work. They could also help address the $92 billion in annual leakage from the retirement system as workers cash out their 401(k)s when changing jobs. These accounts could be a default account to collect those 401(k) balances that get built up in the workplace – especially the “small pots.”

And last—but certainly not least— we think these accounts provide a critical onramp for the Saver’s Match, launching in 2027—a 50% federal match on contributions up to $1,000 annually for lower-income workers, with the potential to benefit up to 69 million people. By channeling those contributions into Trump Accounts, the program could deliver a meaningful boost in retirement savings for the workers who need it most.

Karen: And—because it needs to be said—at the same time, it’s essential that we also recognize that in no way are Trump Accounts a suitable substitute for Social Security. A complement? Yes. But Social Security remains the backbone of retirement security in America, particularly for lower-income workers. There is no substitute for guaranteed, inflation-protected income that you can’t outlive. This needs to be an “and”—not an “or.” We love to see such ambitious policy that could mean real wealth-building for low-wealth households, but let’s be really clear about why these assets need to sit alongside Social Security and other public benefits that provide crucial income supports throughout people’s lives.

We love your thinking – shifting gears -- what worries you right now?

Karen: I worry that disaggregated data is becoming a casualty of the culture wars that are shaping so much of the discourse in American society right now. I’ve been thinking about our years of work with DCIIA and Morningstar to understand precisely how employees use their retirement plans—at the transactional level—and how those usage patterns vary by demographic characteristics in ways that really matter.

If we can’t cut data of various kinds by gender, race, geography, or marital or veteran status, for example, we can’t personalize, or mass-personalize, solutions. And if we don’t personalize, we’re just not building the best outcomes-focused system. We’re just getting started on that frontier, uncovering enormous opportunities to fine-tune retirement savings for so many groups that it just hasn’t worked well for to date, and it’s too important to lose.

It is a sensitive time in that space—you’re not wrong. I think this brings us back to your point about the retirement system needing to work for everyone.

KC: Right. Because ultimately, we get to choose who this system serves. The design choices we make—about access, incentives, and, yes, data—will determine whether the next generation of retirees is more secure than the last. A system this consequential should work for everyone.

Karen and KC, what a terrific conversation, chock full of innovation, inspiration and great ideas. Thank you!

Get or stay connected with Karen and KC. Connect on LinkedIn: Karen Andres and KC Boas. Connect by email: Karen and KC. You can also follow their work at the Aspen Financial Security Program here. You may also be interested in readouts from the Aspen Leadership Forum on Retirement Security – you’ll find the 2025 readout here. You can catch up on past forums here.

As the Director of Inclusive Saving and Investing at the Aspen Institute Financial Security Program, Karen Andres works to spark both policy and market changes that will enable everyone in America to successfully save and invest in assets that grow. KC Boas is the Retirement Savings Initiative Lead at the Aspen Institute Financial Security Program. A longtime advocate for a holistic, people-centered approach to wealth building, KC works across the public and private sectors to develop retirement solutions that benefit all households.

This piece was also featured in the July 17, 2025, edition of Retirement Security Matters. For more fresh thinking on retirement savings innovation, check out the newsletter here.